24.30.4. Tax for Subsidized Services

When a clinic sells taxable items, state tax laws typically require tax to be collected from the purchaser (client), even if a third party (like a nonprofit) is covering the cost of the item. Taxes are not waived simply because the item is subsidized.

How It Works:

When a subsidy or grant is applied to a taxable item:

- The system applies the subsidy to the base price of the item.

- The system charges the client (pet owner) the applicable tax separately.

- This ensures that the clinic collects tax correctly while still allowing the majority of the item to be subsidized.

This setup ensures:

- The nonprofit or grant fund does not pay sales tax.

- The client pays only the legally required tax amount.

- The clinic remains in compliance with applicable state tax laws.

State Tax Law Considerations

Tax laws vary by state. However, most states follow similar rules.

Taxable:

- Tangible goods sold to clients (flea collars, e-collars, prescription and OTC meds, pet food)

- Separately listed items on invoices, even when administered by the veterinarian

Nontaxable (typically):

- Veterinary services (exams, surgery, bundled vaccinations)

- Items used during treatment and not itemized separately

Tip: You can quickly look up your state laws using a Chat GPT summary here

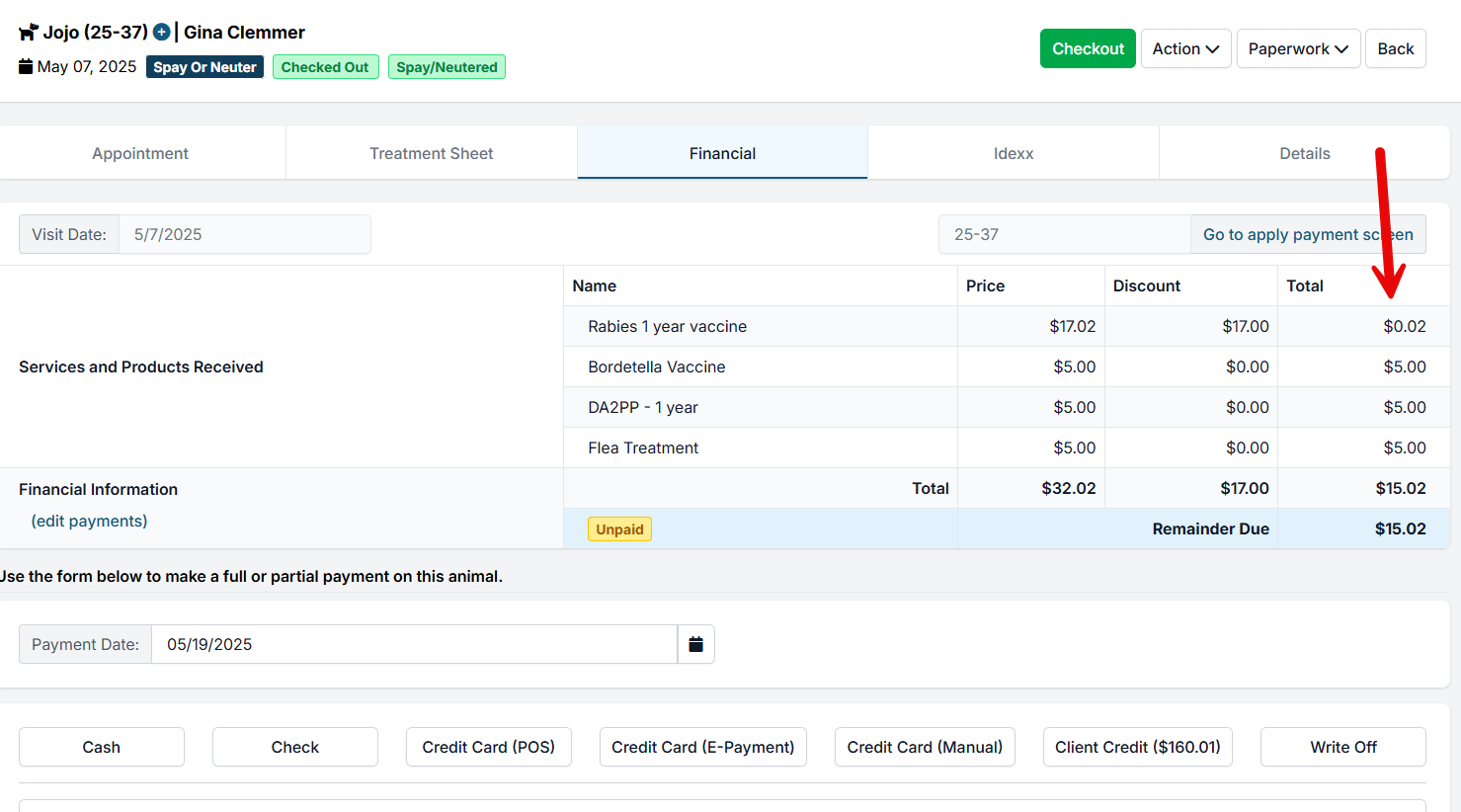

Example: In Minnesota, sales tax must be collected on tangible personal property sold to pet owners—even if a nonprofit is covering the cost. Tax-exempt status applies to purchases made directly by the nonprofit for its own use, not when it funds goods for a third party.

- Item: One-Year Rabies Vaccine

- Price: $17.00

- Sales Tax (MN): $0.02

- Subsidy Applied: $17.00 (paid by grant or nonprofit)

- Client Pays: $0.02 (sales tax only)

Recommendations

- Do not create duplicate invoice items to bypass sales tax.

- Use the system’s existing subsidy tools, which handle taxes correctly.

- Inform clients and funders that a small tax charges may still apply and is legally required.

- Confirm tax obligations with your state’s Department of Revenue if you're unsure.

Benefits of This Approach

- Compliant with state law

- Minimizes manual invoicing errors

- Saves staff time by avoiding duplicate workflows

- Transparent for clients and partners

24.30.3. Sliding Scale Discounts

A subsidy is designed to be inflexible to ensure proper use of grant money and reporting. A subsidy is rigid in its setup and the discount amount or pot deduct amount should not be changed between each use. However, some grants or discounts will require that you offer a discount that is fluid and can change from client to client, or it has a sliding scale on how much the client receives a discount for. To address this, it's best to create multiple subsidies linked to the same funding partnership. Each subsidy setup would offer a different discount amount to clients, for example, Fix Them Voucher ($10 Copay), Fix Them Voucher ($25 Copay), etc. Mix and match the subsidy discount on the services. You can then use the appropriate subsidy for each line item to arrive at the ideal payment total for the client.

24.31. Grantors

In Clinic HQ, you must always indicate the source of a donation—either an individual or an organization.